23 May 2025

National Automobile Olympiad (NAO) 2025 Launch

More Links

New and emerging technologies have had a significant impact on the automotive industry, and in particular, the auto finance and insurance sectors. These technologies are changing the way that consumers buy and finance their vehicles, as well as the way that insurers assess risk and provide coverage. In this blog post, we will examine some of the ways that new and emerging technologies are affecting auto finance and insurance.

The expansion of online financing and sales is one of the most significant ways new technologies affect the auto finance sector. Customers can now completely study and buy cars online, frequently, without ever stepping foot in a dealership.

Many people now find it easier and more convenient to purchase cars because they can research the finest offers and financing alternatives from their homes. Online financing has also made it easier for consumers to compare rates and terms from multiple lenders, increasing competition and driving down interest rates. In addition, many lenders now offer instant approvals and funding, which can considerably speed up car-buying.

Autonomous vehicle development could severely impact the auto insurance and financing sectors. The nature of automobile ownership may alter as self-driving vehicles become more prevalent because consumers may find they no longer need to own a car if they can simply call a self-driving car whenever they need one.

This might result in fewer people owning cars and a move towards more subscription-based business models. Autonomous vehicles also have the potential to reduce the number of accidents on the roads, as they eliminate human error as a factor. This could lead to lower insurance premiums for consumers and lower payouts for insurers. However, it is still unclear how insurance will work for autonomous vehicles, as there are many complex factors to consider, such as liability and cyber-security risks.

Increased risk of cyber attacks: With the rise of connected cars and the Internet of Things (IoT), the risk of cyber attacks on vehicles is becoming a significant concern. Hackers can access sensitive information, such as personal and financial information, and take control of vehicle systems, creating a potential safety risk.

Disruption of traditional models: Introducing new technologies, such as autonomous vehicles and ride-sharing services, can disrupt traditional car ownership and financing models. This disruption may lead to a decline in car ownership, negatively impacting the auto finance and insurance industries.

Personalized pricing models: New technologies such as telematics devices and big data analytics allow insurers to develop more personalized pricing models based on individual driver behavior. This can lead to fairer pricing for drivers and more accurate risk assessments for insurers.

Improved customer experience: The rise of online sales and financing platforms allows for a more streamlined and convenient car-buying experience for customers. This can help to improve customer satisfaction and loyalty.

Blockchain is a decentralized ledger that makes it possible to conduct secure, open transactions without middlemen. By expediting the lending and payment process and lowering the risk of fraud, this technology has the potential to change the auto finance business completely.

Blockchain might be used, for instance, to develop smart contracts that automatically carry out transfers and payments in accordance with predefined criteria, such as the conclusion of a car sale or the payment of a loan installment. This might alleviate the administrative burden on lenders and boost loan process effectiveness.

Big data and analytics are rapidly being employed in the vehicle insurance sector to evaluate risk and anticipate claims. Insurers can learn more about how drivers behave and other elements that might affect risk using data from several sources, including telematics devices, social media, and public records.

Both customers and insurers can gain from using these data to create more precise risk models and pricing schemes. For instance, insurers can utilize data to pinpoint high-risk drivers and modify premiums accordingly, while policyholders may be able to reduce their premiums by practicing safe driving habits.

The future of auto finance and insurance is shaped by emerging technologies, changing consumer preferences, and the need for sustainable transportation solutions. Here are some potential trends and developments that could shape the future of these industries:

Shift to shared ownership and mobility: The traditional paradigm of car ownership is being disrupted by the growth of ride-sharing services and the rising acceptance of car subscription models. With a greater emphasis on offering flexible financing and insurance alternatives for shared mobility models, this trend may cause vehicle finance and insurance companies to change how they conduct business.

Increasing usage of telematics and big data: As more automobiles are connected, the auto finance and insurance industries will frequently employ telematics devices and big data analytics. Moreover, it will enable more precise risk evaluations, claim processes, and individualized pricing models.

Sustainability is receiving more attention as consumers and policymakers call for more sustainable transportation options in response to the growing worry over climate change. By providing financing and insurance choices for environmentally friendly automobiles and investing in green technologies and procedures, auto finance and insurance firms must adjust to this trend.

The impact of new and emerging technologies on auto finance and insurance is substantial, with both challenges and opportunities for the industry. Online financing and sales have made it easier for consumers to buy cars and compare rates, while autonomous vehicles have the potential to reduce accidents and lower insurance premiums.

However, there are challenges, such as the increased risk of cyber attacks and the disruption of traditional models. Blockchain and big data analytics are also expected to play a significant role in the future of auto finance and insurance, allowing for more secure and precise transactions and risk assessments. The industry must also adapt to changing consumer preferences, such as the shift towards shared ownership and mobility and the growing demand for sustainable transportation options.

National Automobile Olympiad (NAO) 2025 Launch

Bharat Mobility Expo 2025

PM Solar 2EV Project for social justice

Bharat Mobility Expo 2024

Annual Conclave 2023

G-20 Jan Bhagidaari Webinar On 6th June 2023 at 11:00 AM to 12:00 PM

We would be pleased to receive you at the Auto Expo Components Show scheduled from 13-18 January 2023 at the India Expo Mart, Greater Noida , Utter Pradesh, Delhi NCR

We would be pleased to receive you at the Auto Expo Components Show scheduled from 12-15 January 2023 at the Pragati Maidan, New Delhi.

8th IVASS

Pradhan Mantri National Apprenticeship Mela

Swavalamban Skill to Enterprise Model (STEM Flyer 1)

Swavalamban Skill to Enterprise Model (STEM Flyer 2)

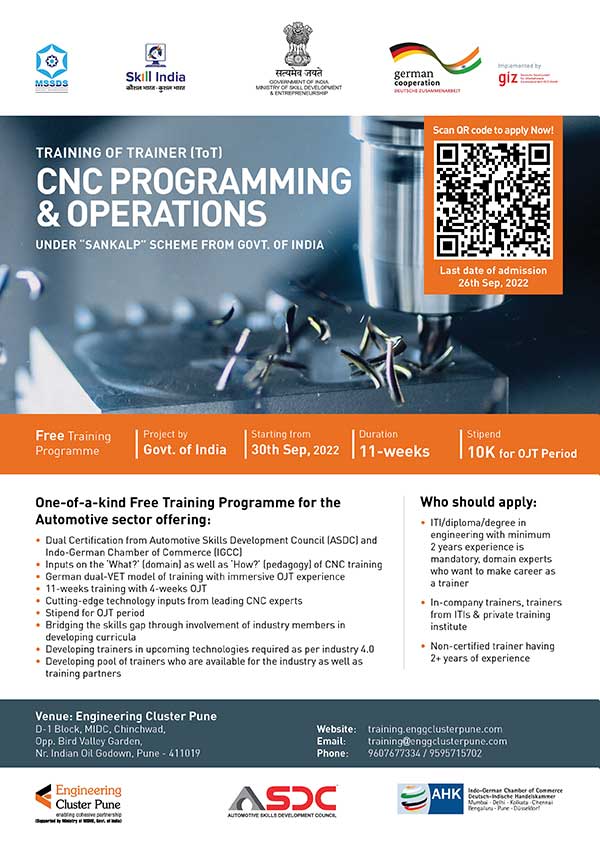

CNC Programming & Operation

Annual Conclave 2022

Launch of project

ASDC Collaborates with power SSC

Glimpes of RTI visit Kakinada

Glimpses From FDP Inaugration For EV Technology at AKGEC

Introductory Workshop

Kolkata Job Fair

TeamLease Degree Apprenticeships on significance of dgree Apprenticeship Program in building Talent Pipeline

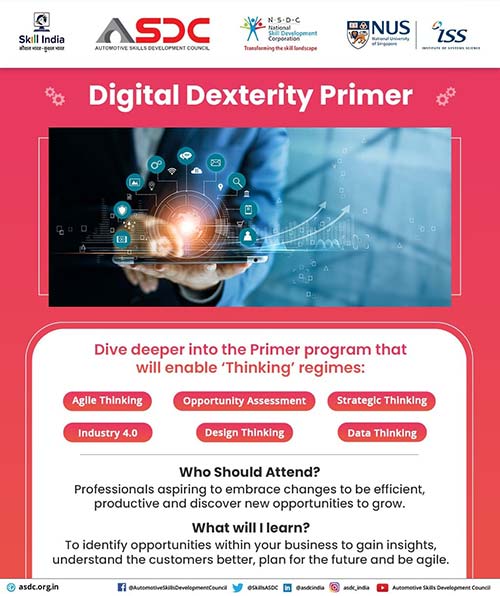

Digital Dexterity Primer

CMIA's Energy Conclave 2022

We are now associated with ISS, National University of Singapore for the Digital Dexterity Primer program to help enhance the digital business approach among auto professionals. Register now and get equipped with required skills and insights to cater to y

We are proud to be associated with Grwp Colegau NPTC Group of Colleges for the Training of Trainers on Electric Vehicle Service Lead Technician course. The aim of the e-learning course is to upskill auto professionals and students with valuable electric v

We look forward to you joining our prolific speakers for Women’s Day Webinar on ‘Careers in Automotive sector for women: Challenges and Opportunities’.

ASDC invites you all to EV India 2021 An Electric Motor Vehicle show

ASDC Annual Conclave and Livestreaming on 28th sept 3 pm onwards

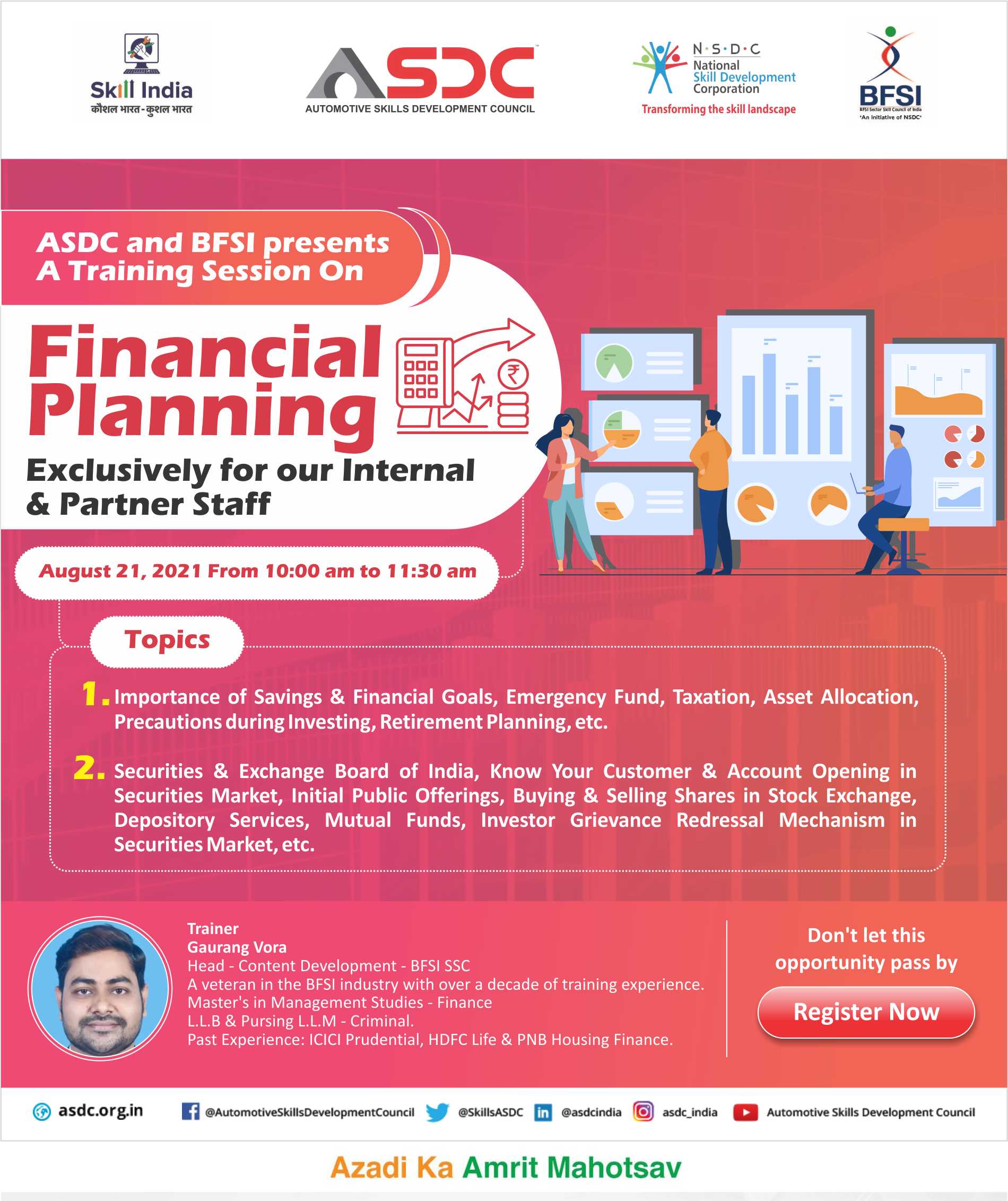

ASDC along BFSI will be hosting a training session on Financial Planning for its Internal and Partner staff on Saturday , August 21 from 10 - 11:30 am . The session would be conducted by Gaurang Vohra, Head of Content Development at BFSI SSC. His decade l

ASDC & Tata Strive will be conducting a free online refresher program on ‘Being a superstar facilitator - Kolb's Experimental learning cycle ’ to upskill the auto workforce, on 2nd August from 3-4pm

ASDC & Tata Strive will be conducting a free refresher ToT program on ‘Power Assisted Steering (Hydraulic & Electronic)’ to upskill the auto workforce, on 30th July from 3-4pm

Hon'ble Prime Minister Shri Narendra Modi will be addressing the nation LIVE on the completion of one year of transformative reforms under NEP 2020, on 29th July, 2021 at 4:30 PMs

Earn an accredited Diploma Degree without quitting your job at ZERO COST*

WORLD YOUTH SKILLS DAY

Reimagining Youth Skills in India – Post Pandemic

July 15, 2021 | 1500 hrs

Join the Nation's Premier gathering of Academicians, Education Practioners, Industry Experts and Leaders for exchanging result-based solution..........

Join trailblazers from the Indian #Automobile Industry during SIAM's lecture session on 'EV in India...

Here’s an exclusive opportunity for final Year engineering students to interact live with Mr. Arindam Lahiri, CEO, ASDC

Online Workshop to Gain Perspectives on Structure and Curriculum element for training Cluster Based Trainees(TOT) Under Sankalp

Importance of standards & Skilling in the Automotive Electronics Industry

Next Step Pane Series

Launch Of Talk Show - Safer Drives Mission Possible

2nd Phase of Grow with Google

Digitising Indian Auto Retail

Grow With Google : Grow with Google is excited to bring you a three-part webinar series on "Digitising Indian Auto Retail" powered by ASDC & FADA.”

6th IVASS - India Vehicle After Sales Summit

Engaging skilled Service Technician Through National Apprenticeship Promotion Scheme (NAPS)

Webinar on Boosting Green Economy Is E mobility the way forward in Rajasthan

Welding Technician, Online Course

Auto Serve 2020 is back! Join us at India's most trusted exhibition and trade fair from 23rd Nov’20.

9th edition of AutoServe2020 organized by the Confederation of Indian Industry

ASDC- RPL-1 training & assessment program at Skillsource Learning and Technologies training Centre in NTI Moradabad, Uttar Pradesh

Managing the changing skills demand in a global industry

Exclusive SSC Webinar: Join to discuss and learn from experts on Adult Digital Learning

Webinar on Employment Opportunities During COVID -19 during 4pm - 5:30pm on Thursday , 10th Sept 2020

ACMA 60th Annual Session(Virtual), 09: 30 hrs: September 05, 2020

Join us as we drive into the #newnormal for the Auto Industry with our presenting partner @audi_mumbaiwest

9th HR Conclave Re -Emerging in New Normal

Virtual job Fair 2020

Skills -Deficit faced by Industry and Youth employability Issue

E-Learning course offered by carmate in association with NATRAX and certification partner ASDC

Mr. Arindham Lahiri, CEO, ASDC Co-Moderator at PManifold Webinar

Upskilling EV Industry in India: Product Design, Testing and Calibration

World Youth Skills Day

Digital Sales Master Class

REBOOT : Let's Talk Intelligent Manufacturing

Bengal National Chamber of Commerce and Industry and National Skill Development Corporation in association with 2COMS present an online session on Post Covid- Scope and Reforms in Apprenticeship for Industry 4.0.

Join the conversation with Mr. Nikunj Sanghi, Chairman-ASDC, and Mr. Singhvi, Chairman- ACMA India, Skilling Pillar & Treasurer –ASDC along with the other prominent industry leaders at the Rajasthan Skills Summit organized by FICCI Rajasthan

Training of Master Trainer : Service Domain

5th July webinar: Emerging Skills Amid Disruptions in the Automobile Industry

Digital Master Class Launch for Automotive dealerships

Virtual INTERNATIONAL AUTOMOTIVE MANUFACTURING SUMMIT 2020 Manufacturing Excellence post-Lockdown

The ASDC tellecaller -Auto Dealership Online Course

Digital Training of Trainers Program : Sales executive dealership

Mr. @nikunjsanghi, Chairman– ASDC, will be one of the esteemed panellists at the webinar organized by @myfirstboss1 on 8th May 2020

Mr. ARINDAM LAHIRI, CEO - ASDC, will be one of the key speakers at the webinar. Register now

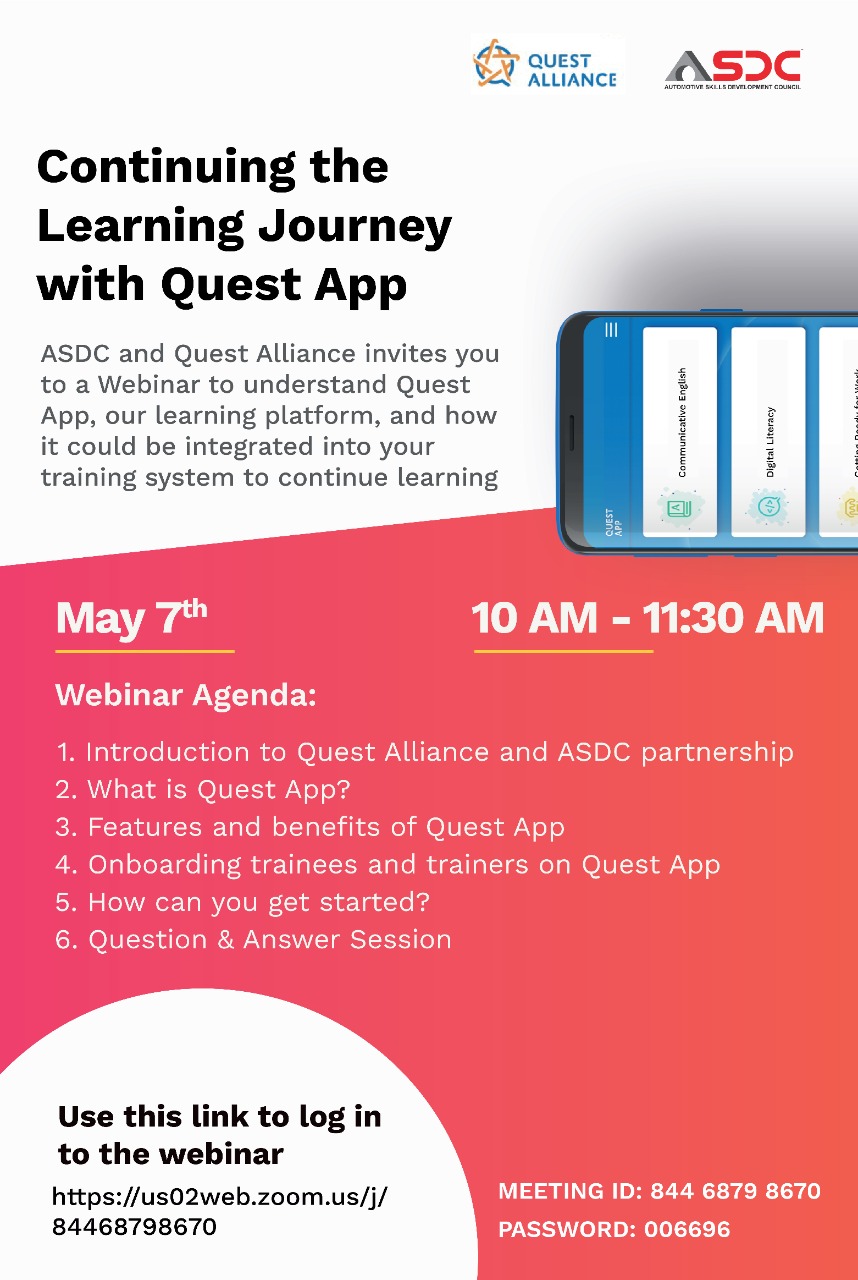

Continuing the Learning journey with Quest App : 7th May, 10 AM to 11:30 AM

COVID-19 impact on Manufacturing and Skilling.

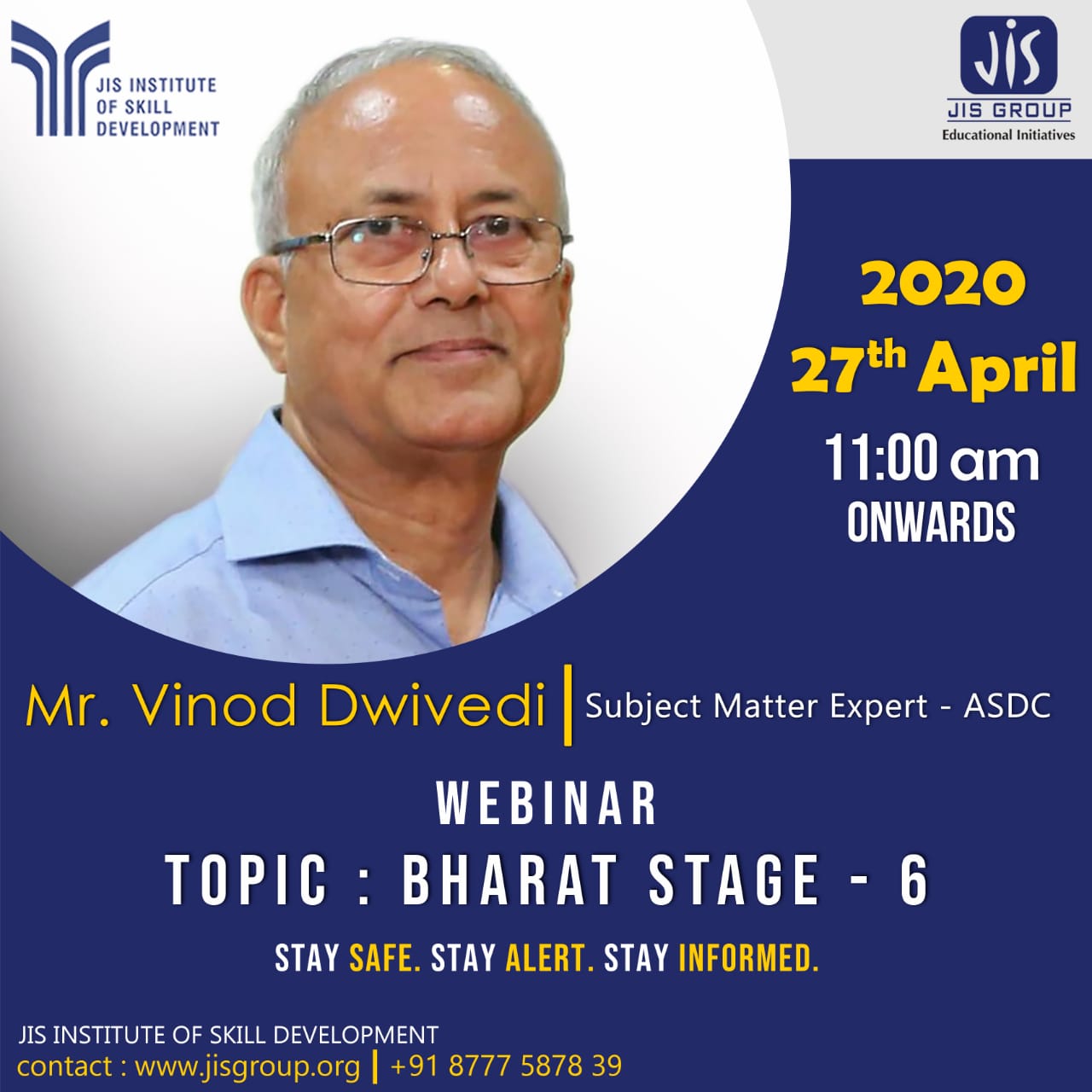

Technilological changes in Bharat Stage 6 (BS VI) vehicles Session by SME , ASDC Time: Apr 27, 2020 11:00 AM Mumbai, Kolkata, New Delhi

Knowledge plus Certification. Sat April 25, 11 AM to 5 PM. The Best Investment for your Career. Block your Slot Now.

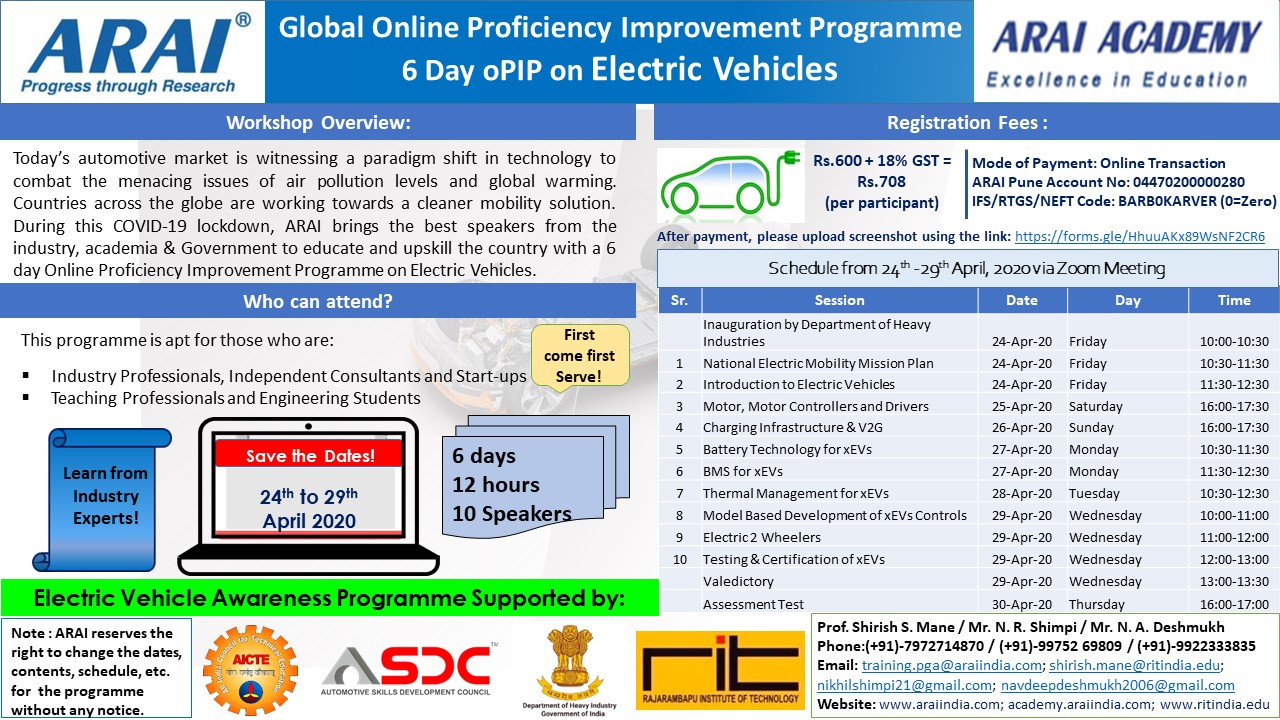

Velidictory Function for the 6 Day Global Online Proficiency Improvement Programme (oPIP) from 24th – 29th April 2020

Join the stalwarts of the Automotive Industry in a spirited discussion on 23rd April Time: 5:00 PM

ASDC Annual Conclave 2019

Partners’ Forum 2019

India's electric vehicle transition has crossed from aspiration into reality. As of early 2026, the PM E-DRIVE Scheme has supported more than 28 lakh EVs, with 22.12 lakh units sold as of January 2026.

The automotive industry is undergoing its most significant structural shift in over a century. Across the world, OEMs are retooling factories, rewriting production playbooks, and rethinking their workforce requirements as electric vehicles move from niche products to mainstream manufacturing priorities.

The auto industry in India is racing toward electrification, connectivity and automation. New automotive jobs will center on electric vehicles (EVs), software and advanced electronics.

The Indian auto sector is undergoing a rapid transformation. Electric vehicles (EVs), connected car technology, and advanced driver-assistance systems (ADAS) are reshaping the landscape.

Automotive industry is currently experiencing a historic transformation. With the market projected to reach $300 billion by 2026, the demand for high-precision manufacturing has never been higher

The BW Auto World 40 Under 40 Summit & Awards 2025 brought together industry leaders, policy makers, and young innovators at a defining moment for India’s automotive sector.