23 May 2025

National Automobile Olympiad (NAO) 2025 Launch

More Links

When considering a new or used vehicle, one of the first decisions you'll need to make is how to finance it. There are two main options: a loan or a lease. When it comes to buying a car, there are a few different financing options to choose from: a loan or a lease. Both have their advantages and drawbacks, so it’s essential to understand the differences before deciding.

With a car loan, you’ll borrow a set amount of money from a lender and then pay that back over a set period of time, usually three to five years. At the end of the loan, you’ll own the car outright.

Introduction to auto financing

When you are looking to buy a new or used car, one of the decisions you will have to make is how to finance the purchase. There are a few different options available, and the one you choose will depend on your individual circumstances. This guide will introduce you to the basics of auto financing and help you decide which option is best for you.

The difference between loans and leases

There are a few key differences between loans and leases when it comes to auto finance.

When you take out a loan, you are borrowing money from a lender in order to purchase a car. You will then make monthly expenses to pay back the loan, plus interest & Once you have spent off the loan, you will own the car.

When you lease a car, you borrow the car from the dealership or leasing company for a set period. You will make monthly payments, and at the end of the lease you have the option to either buy the car or lease another car.

The pros and cons of loans

When it comes to taking out a loan, there are a lot of pros and cons to consider.

Pros

You can get the money you need to finance a big purchase or project.

A loan can help you build your credit history.

A loan can support you consolidate your debts.

A loan can help you start or grow a business.

You could end up spending more in interest than the amount you borrowed.

You have to pay it back, with interest.

You may end up paying more in interest and have to commit to a longer repayment term.

You may have to put up your private assets as collateral.

Ultimately, the decision to take out a loan is a personal one. Weigh the pros and cons carefully to see if a loan is a right choice for you.

The pros and cons of leases

Pros

Leases are a great way to avoid the large down payment often required to purchase a car

They also offer a low monthly payment and the convenience of turning in the car at the end of the lease.

Leasing is a great way to get into a new car without breaking the bank.

you are limited in the number of miles you can drive each year without incurring additional charges.

you are responsible for any damages that occur to the car during the lease term.

you will have to turn the car back in to the dealer at the end of the lease, even if you still owe money on it.

When you are looking to buy a car, you will have to decide whether to take out a loan or lease the car. There are pros and cons to both options, so you will need to decide which is best for you.

If you take out a loan, you will own the car outright and you will be responsible for making all the payments on the loan. This can be a good option if you want to be able to sell the car at any time and you want to build up your own equity in the car. However, you will need to be able to afford the monthly payments, which can be expensive.

If you lease the car, you will not own it, but you will have to pay for only the portion of the car that you use. This can be a good option if you don't want to be responsible for car payments or don't have much money to spend on a car. However, you will not be able to sell the car at any time and will not build any equity in it.

How to get the best deal on a loan or lease

There are a lot of factors to consider when trying to get the best deal on an auto loan or lease. You need to think about the car you want, the terms of the loan or lease, and your credit score.

When you're looking for a car, it's important to consider what you can afford. You don't want to overspend on a car and end up with a high monthly payment. You also need to think about the terms of the loan or lease. You may want to consider a shorter loan or lease term so you can get into a new car more often.

Your credit score is also important when it comes to getting the most suitable deal on a car & Lenders will look at your credit score to determine how risky it is to lend you money. If you have a good credit score, you may be able to get a lower interest rate on your loan or lease.

FAQs

Q: What is the difference between a car loan and a car lease?

A car loan is when you borrow money from a lender in order to buy a car. A car lease is when you borrow money from a lender in order to rent a car.

Q: What are the benefits of a car loan?

The benefits of a car loan include:

-You can buy a car that is more expensive than you could afford if you were only leasing it.

-You can keep the car for as long as you want, as long as you continue to make your payments.

-You can sell the car whenever you want and keep the money from the sale.

Q: What are the benefits of a car lease?

The benefits of a car lease include:

-You can lease a car for a lower monthly payment than you would pay for a car loan.

-You can often get a newer car than you could if you were buying it.

National Automobile Olympiad (NAO) 2025 Launch

Bharat Mobility Expo 2025

PM Solar 2EV Project for social justice

Bharat Mobility Expo 2024

Annual Conclave 2023

G-20 Jan Bhagidaari Webinar On 6th June 2023 at 11:00 AM to 12:00 PM

We would be pleased to receive you at the Auto Expo Components Show scheduled from 13-18 January 2023 at the India Expo Mart, Greater Noida , Utter Pradesh, Delhi NCR

We would be pleased to receive you at the Auto Expo Components Show scheduled from 12-15 January 2023 at the Pragati Maidan, New Delhi.

8th IVASS

Pradhan Mantri National Apprenticeship Mela

Swavalamban Skill to Enterprise Model (STEM Flyer 1)

Swavalamban Skill to Enterprise Model (STEM Flyer 2)

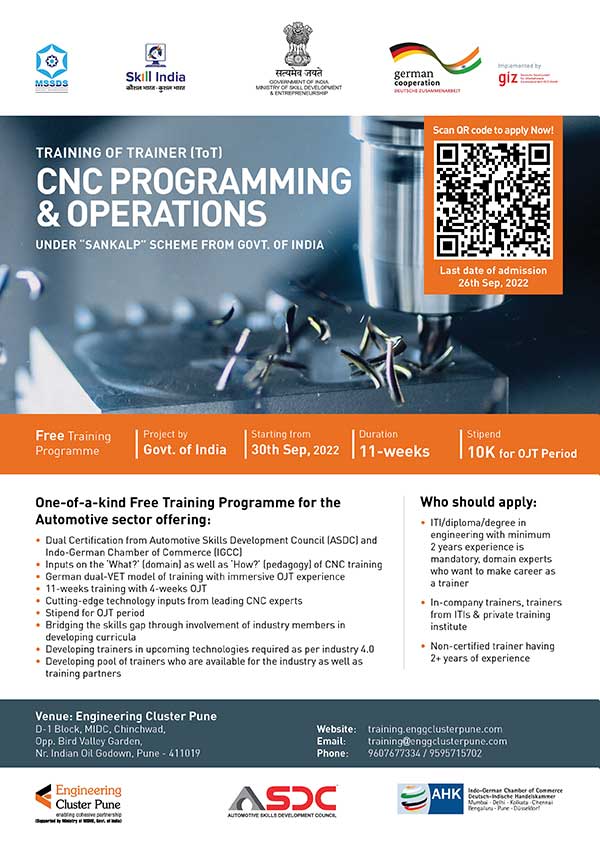

CNC Programming & Operation

Annual Conclave 2022

Launch of project

ASDC Collaborates with power SSC

Glimpes of RTI visit Kakinada

Glimpses From FDP Inaugration For EV Technology at AKGEC

Introductory Workshop

Kolkata Job Fair

TeamLease Degree Apprenticeships on significance of dgree Apprenticeship Program in building Talent Pipeline

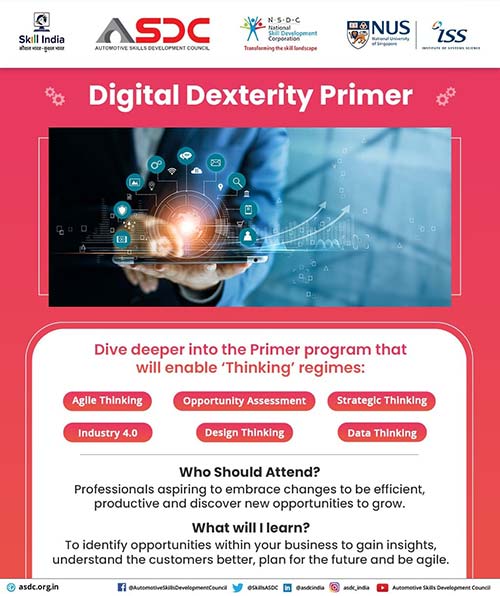

Digital Dexterity Primer

CMIA's Energy Conclave 2022

We are now associated with ISS, National University of Singapore for the Digital Dexterity Primer program to help enhance the digital business approach among auto professionals. Register now and get equipped with required skills and insights to cater to y

We are proud to be associated with Grwp Colegau NPTC Group of Colleges for the Training of Trainers on Electric Vehicle Service Lead Technician course. The aim of the e-learning course is to upskill auto professionals and students with valuable electric v

We look forward to you joining our prolific speakers for Women’s Day Webinar on ‘Careers in Automotive sector for women: Challenges and Opportunities’.

ASDC invites you all to EV India 2021 An Electric Motor Vehicle show

ASDC Annual Conclave and Livestreaming on 28th sept 3 pm onwards

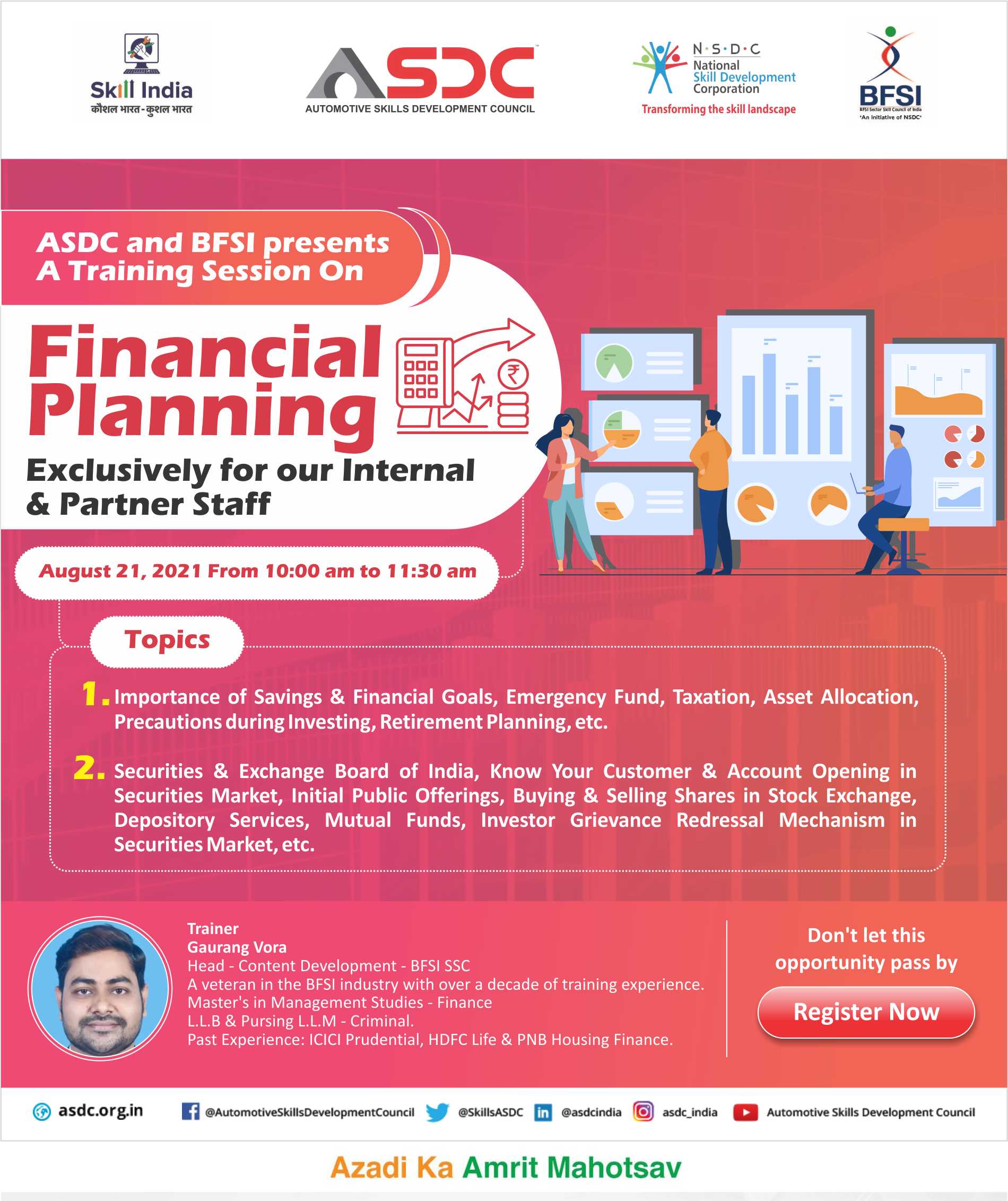

ASDC along BFSI will be hosting a training session on Financial Planning for its Internal and Partner staff on Saturday , August 21 from 10 - 11:30 am . The session would be conducted by Gaurang Vohra, Head of Content Development at BFSI SSC. His decade l

ASDC & Tata Strive will be conducting a free online refresher program on ‘Being a superstar facilitator - Kolb's Experimental learning cycle ’ to upskill the auto workforce, on 2nd August from 3-4pm

ASDC & Tata Strive will be conducting a free refresher ToT program on ‘Power Assisted Steering (Hydraulic & Electronic)’ to upskill the auto workforce, on 30th July from 3-4pm

Hon'ble Prime Minister Shri Narendra Modi will be addressing the nation LIVE on the completion of one year of transformative reforms under NEP 2020, on 29th July, 2021 at 4:30 PMs

Earn an accredited Diploma Degree without quitting your job at ZERO COST*

WORLD YOUTH SKILLS DAY

Reimagining Youth Skills in India – Post Pandemic

July 15, 2021 | 1500 hrs

Join the Nation's Premier gathering of Academicians, Education Practioners, Industry Experts and Leaders for exchanging result-based solution..........

Join trailblazers from the Indian #Automobile Industry during SIAM's lecture session on 'EV in India...

Here’s an exclusive opportunity for final Year engineering students to interact live with Mr. Arindam Lahiri, CEO, ASDC

Online Workshop to Gain Perspectives on Structure and Curriculum element for training Cluster Based Trainees(TOT) Under Sankalp

Importance of standards & Skilling in the Automotive Electronics Industry

Next Step Pane Series

Launch Of Talk Show - Safer Drives Mission Possible

2nd Phase of Grow with Google

Digitising Indian Auto Retail

Grow With Google : Grow with Google is excited to bring you a three-part webinar series on "Digitising Indian Auto Retail" powered by ASDC & FADA.”

6th IVASS - India Vehicle After Sales Summit

Engaging skilled Service Technician Through National Apprenticeship Promotion Scheme (NAPS)

Webinar on Boosting Green Economy Is E mobility the way forward in Rajasthan

Welding Technician, Online Course

Auto Serve 2020 is back! Join us at India's most trusted exhibition and trade fair from 23rd Nov’20.

9th edition of AutoServe2020 organized by the Confederation of Indian Industry

ASDC- RPL-1 training & assessment program at Skillsource Learning and Technologies training Centre in NTI Moradabad, Uttar Pradesh

Managing the changing skills demand in a global industry

Exclusive SSC Webinar: Join to discuss and learn from experts on Adult Digital Learning

Webinar on Employment Opportunities During COVID -19 during 4pm - 5:30pm on Thursday , 10th Sept 2020

ACMA 60th Annual Session(Virtual), 09: 30 hrs: September 05, 2020

Join us as we drive into the #newnormal for the Auto Industry with our presenting partner @audi_mumbaiwest

9th HR Conclave Re -Emerging in New Normal

Virtual job Fair 2020

Skills -Deficit faced by Industry and Youth employability Issue

E-Learning course offered by carmate in association with NATRAX and certification partner ASDC

Mr. Arindham Lahiri, CEO, ASDC Co-Moderator at PManifold Webinar

Upskilling EV Industry in India: Product Design, Testing and Calibration

World Youth Skills Day

Digital Sales Master Class

REBOOT : Let's Talk Intelligent Manufacturing

Bengal National Chamber of Commerce and Industry and National Skill Development Corporation in association with 2COMS present an online session on Post Covid- Scope and Reforms in Apprenticeship for Industry 4.0.

Join the conversation with Mr. Nikunj Sanghi, Chairman-ASDC, and Mr. Singhvi, Chairman- ACMA India, Skilling Pillar & Treasurer –ASDC along with the other prominent industry leaders at the Rajasthan Skills Summit organized by FICCI Rajasthan

Training of Master Trainer : Service Domain

5th July webinar: Emerging Skills Amid Disruptions in the Automobile Industry

Digital Master Class Launch for Automotive dealerships

Virtual INTERNATIONAL AUTOMOTIVE MANUFACTURING SUMMIT 2020 Manufacturing Excellence post-Lockdown

The ASDC tellecaller -Auto Dealership Online Course

Digital Training of Trainers Program : Sales executive dealership

Mr. @nikunjsanghi, Chairman– ASDC, will be one of the esteemed panellists at the webinar organized by @myfirstboss1 on 8th May 2020

Mr. ARINDAM LAHIRI, CEO - ASDC, will be one of the key speakers at the webinar. Register now

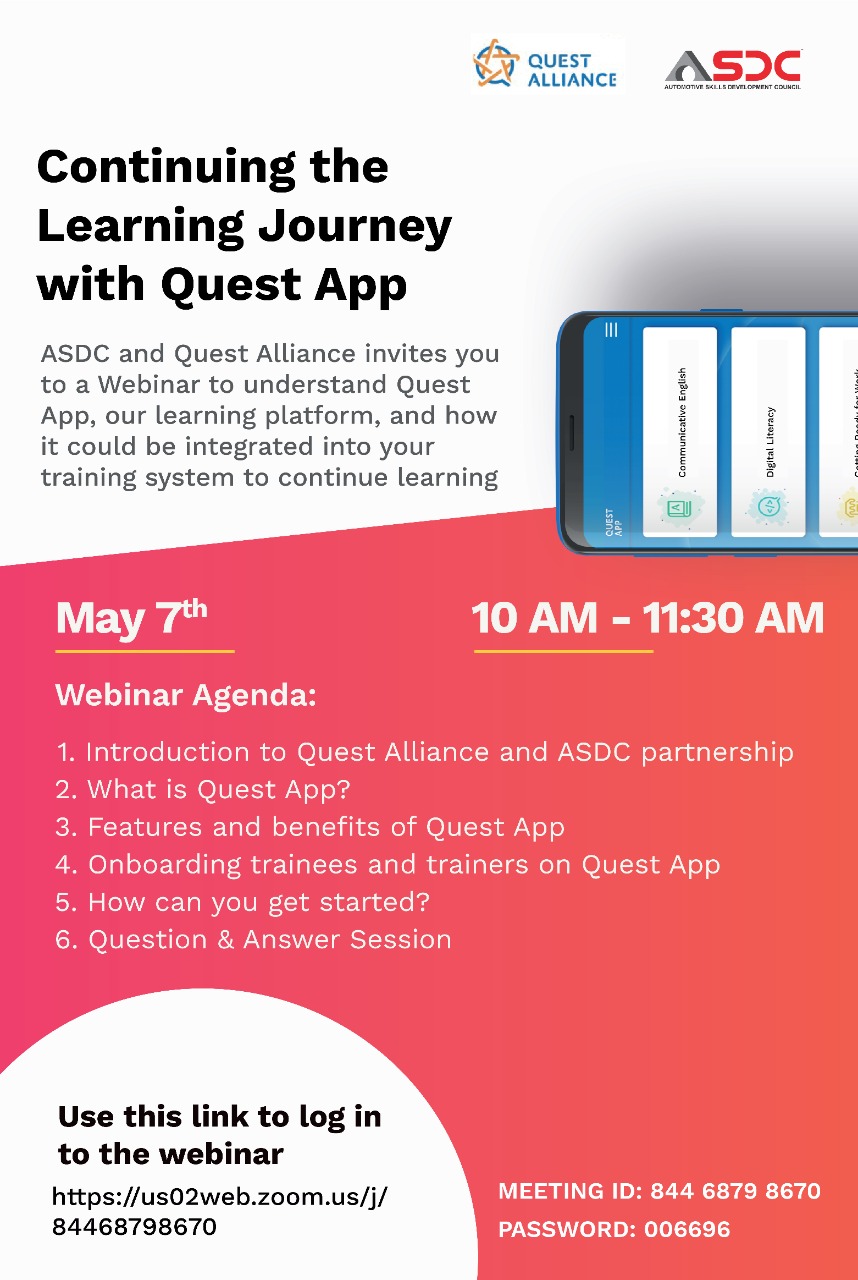

Continuing the Learning journey with Quest App : 7th May, 10 AM to 11:30 AM

COVID-19 impact on Manufacturing and Skilling.

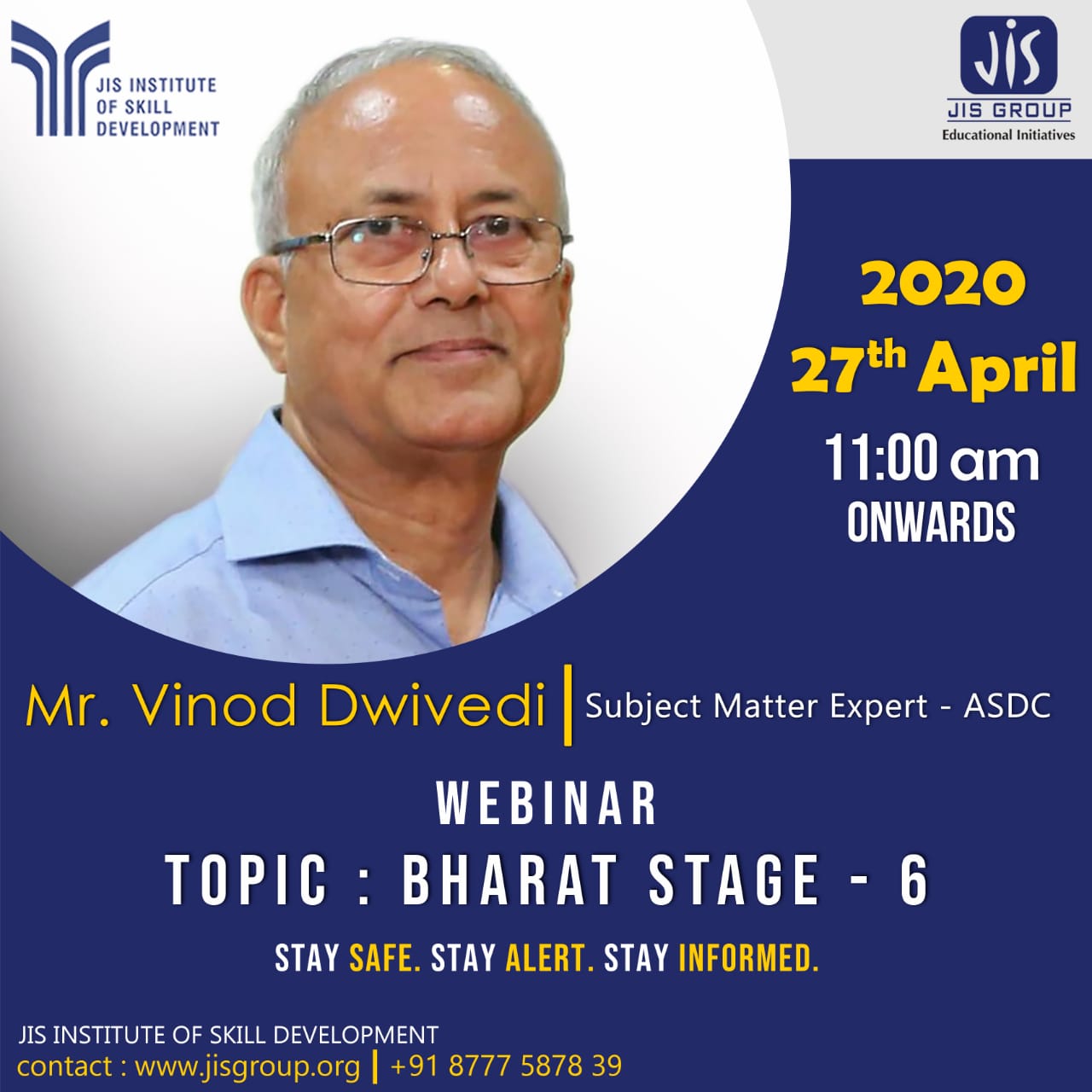

Technilological changes in Bharat Stage 6 (BS VI) vehicles Session by SME , ASDC Time: Apr 27, 2020 11:00 AM Mumbai, Kolkata, New Delhi

Knowledge plus Certification. Sat April 25, 11 AM to 5 PM. The Best Investment for your Career. Block your Slot Now.

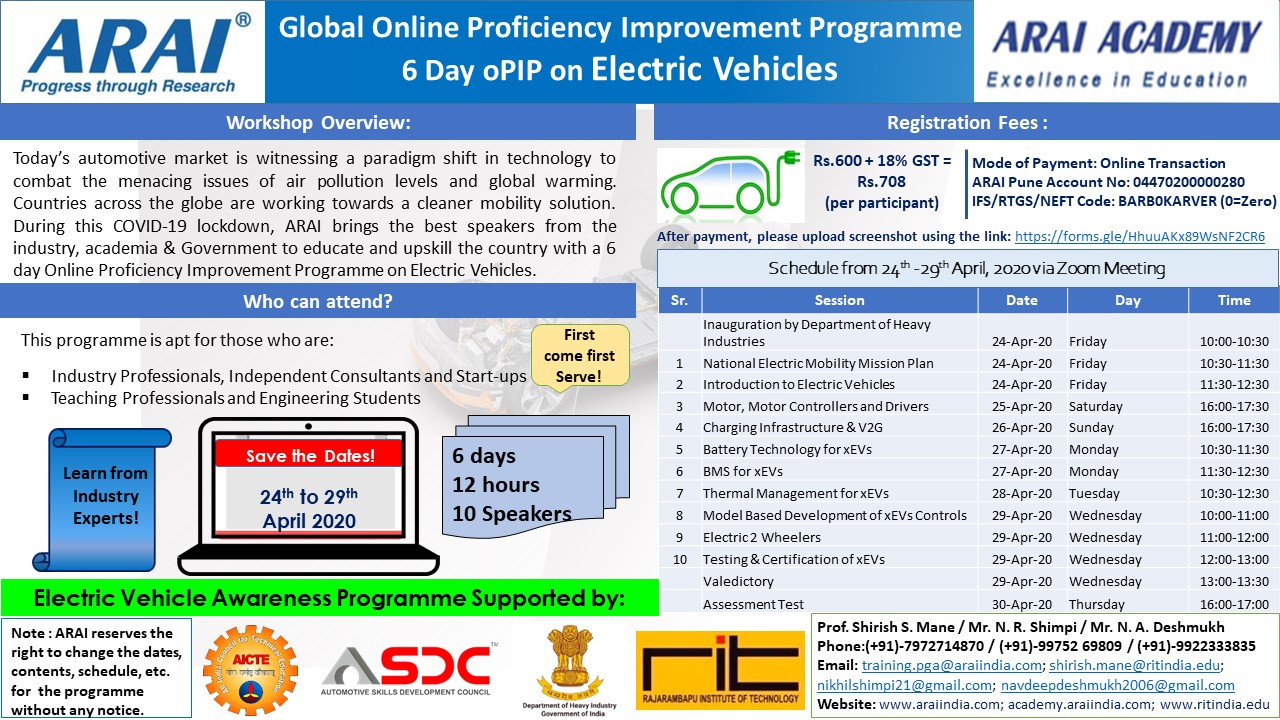

Velidictory Function for the 6 Day Global Online Proficiency Improvement Programme (oPIP) from 24th – 29th April 2020

Join the stalwarts of the Automotive Industry in a spirited discussion on 23rd April Time: 5:00 PM

ASDC Annual Conclave 2019

Partners’ Forum 2019

India's electric vehicle transition has crossed from aspiration into reality. As of early 2026, the PM E-DRIVE Scheme has supported more than 28 lakh EVs, with 22.12 lakh units sold as of January 2026.

The automotive industry is undergoing its most significant structural shift in over a century. Across the world, OEMs are retooling factories, rewriting production playbooks, and rethinking their workforce requirements as electric vehicles move from niche products to mainstream manufacturing priorities.

The auto industry in India is racing toward electrification, connectivity and automation. New automotive jobs will center on electric vehicles (EVs), software and advanced electronics.

The Indian auto sector is undergoing a rapid transformation. Electric vehicles (EVs), connected car technology, and advanced driver-assistance systems (ADAS) are reshaping the landscape.

Automotive industry is currently experiencing a historic transformation. With the market projected to reach $300 billion by 2026, the demand for high-precision manufacturing has never been higher

The BW Auto World 40 Under 40 Summit & Awards 2025 brought together industry leaders, policy makers, and young innovators at a defining moment for India’s automotive sector.